Series A - My Investment Thesis

First Series A deal that we closed as a lead investor since I started to work with Xavier Niel

We invest in about 100 new deals per year with Kima Ventures. Mainly seed deals, EU & US, as lead or follower. Our main focus is the learning and execution curve of the team applied to a market opportunity that we like. The rest is conviction under 90% of uncertainty.

In the meantime, we’ve recently looked at a bunch of companies that were raising Series A deals. I’ve worked a lot on my investment thesis the past years to narrow my sweet spot and build a consistent approach towards Series A deals in Europe. To provide you with a more concrete view of the companies I’ve been really excited about recently, here is a list of the ones that we funded:

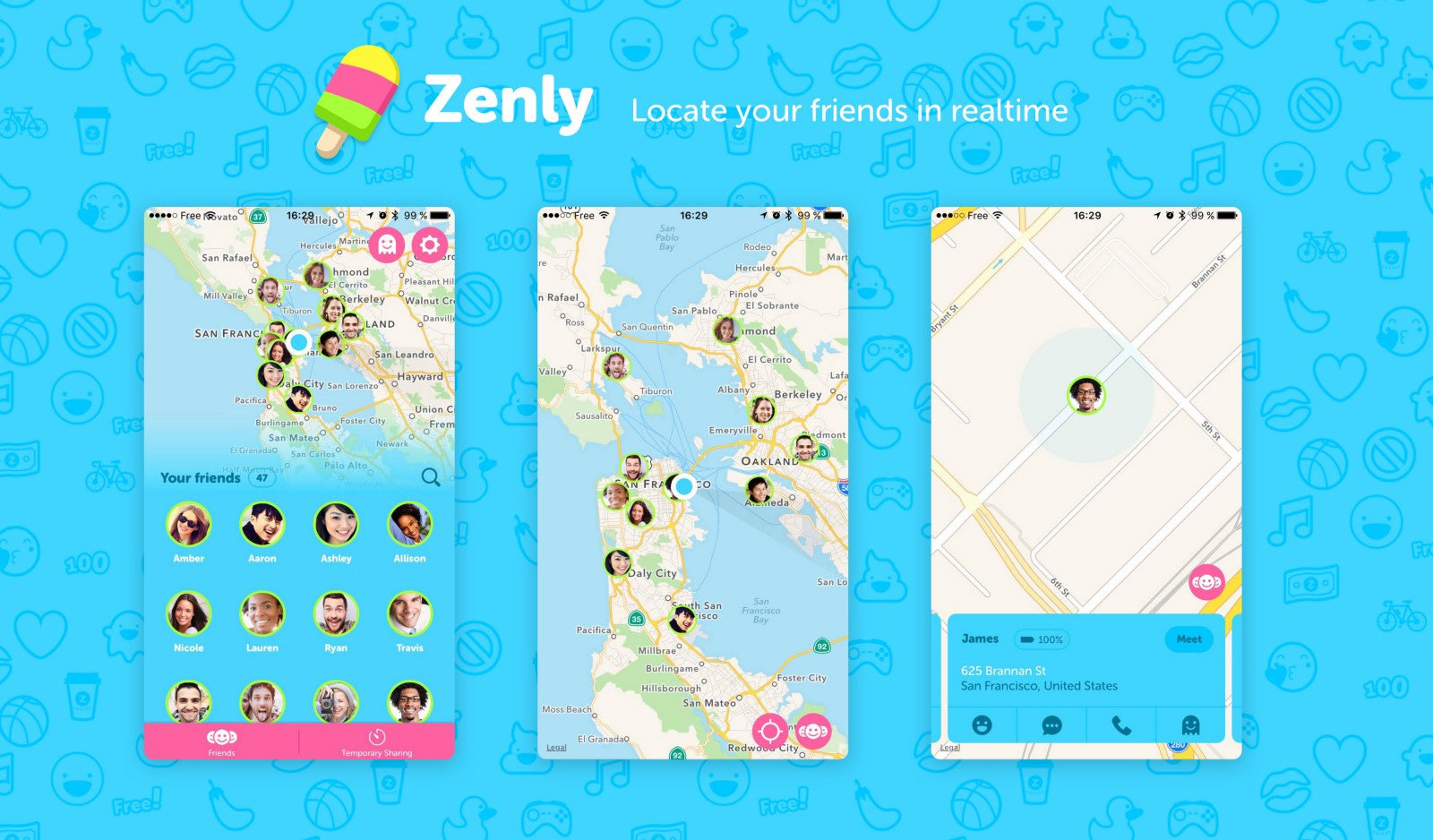

Zen.ly : Your friends, in real life.

Sourced.tech : Building the technological stack for AI on code.

Payfit.com : Payroll management, automagically.

Ibanfirst.com : The European inter-banking platform for businesses.

Side.co: A new work experience for flexible jobs. (edit May 2017)

Forestadmin.com: The admin interface your team deserves (edit Jan 2018)

My investment thesis for those series A deals is based on the following pillars (considering that the market opportunity is huge of course):

The founding team has demonstrated its capacity to hire and manage an A-team of at least 15 people and as I conduct interviews with every single employee to assess the quality of team, I easily extrapolate a solid culture and organisation in the making that will be able to sustain hundreds of people.

Their technological layer or product approach is way beyond the market standards and the competition, providing them with a defensive and strong competitive advantage.

The CEO has the extraordinary ability to present an ambitious future of where they (and the market) are heading to that sounds brillant yet obvious while no one had never envisioned it before.

In terms of business stage, I usually bet on those companies post initial traction but pre-acceleration. And because of this unique setup:

We provide them with more money than the venture capital market would tend to provide them at the time of the investment even though it increases the valuation.

We tend to bet on those companies 6 to 12 months before any other institutional investors. It also allows to drive attention around the deal and put the company’s self-fulfilling prophecy at work :)

To provide this companies with more money, sooner in their equity story, allows them to keep the right focus, to increase their velocity and to fuel their ambition.

Cheers :)